Most people cannot live on Social Security or a pension alone. Investing and saving for the future in retirement accounts, like 401 k s or IRAs , is key to funding a long and happy retirement. But this begs the question of what should you be invested in? In the news , we hear a lot about the outperformance of certain tech companies like Apple, Amazon, Facebook, and Microsoft. Does it still make sense to diversify in today’s investment environment? We believe the answer is a resounding yes, and the most recent quarter helps exemplify that fact.

What is the purpose of diversification?

The idea behind diversification is to invest your money in a variety of different asset classes. This way you have exposure to various areas of the stock market, so everything is not going up, or down, at the same rate at the same time. You spread out your risk, so you are invested in certain areas when they are p er forming well and are not entirely invested in them when they are performing poorly.

Levels of diversification

When looking to diversify an investment portfolio, there are various levels to examine . At each level, the investment s are reviewed in increasing detail , like how looking through a microscope provides a more detailed picture of what you are viewing.

1) Stocks vs. bonds:

At the highest level of viewing diversification is the split between stocks and bonds. M ore simply put, “risky” assets vs. more “stable” assets. The “stock” portio n of someone’s investment portfolio would also likely include things such as crypto currencies or Real Estate Investment Trusts (REITs), although these are not necessarily “stocks” but are volatile assets. While on the bond side you would also include things like cash or CDs since these items do not tend to fluctuate very much.

Generally, the very first decision you need to make is to determine how you want to allocate your investments between stocks and bonds. Once this overarching decision has been mad e you can then get more granular about other diversification decisions.

2) Asset classes

The next decision is to decide how you want to allocate your various stocks and bonds by placing them in different asset classes. On the stock side, this might include things like large US (United States) companies, small US companies, international stocks, emerging market stocks, REITs, etc. For bonds, this may include US government bonds, corporate bonds, mortgage-backed bonds, international bonds, etc.

Determining the asset classes to hold breaks down your investment portfolio further and doing so can provide additional diversification to your overall investments.

3) Subcategories

If you thought choosing asset classes are not enough, you can go even further and break down those asset classes into subcategories . For stocks, a common subcategory to consider is value vs. growth funds. At a high level, this refers to the valuation of a various company (or group of companies). Value stocks have a lower price to earnings or price to book ratio , and as the name implies, are considered a value (on sale), at least based on this metric. Growth stocks on the other hand have a higher valuation metric but tend to be increasing their revenue s faster than value companies, with the expectation that their “growth” will continue to accelerate in the future.

Bonds also have various subcategories to consider inside of their overarching asset class. A couple common metrics include credit quality and time to maturity (or more importantly duration). The higher the credit rating of a bond the “safer” it is deemed to be, and the more likely you are to receive the expected interest payment and principal back when the bond matures (is finished). In theory, t he “safer” the bond the lower the interest payment you will receive (a tradeoff of risk vs. reward). Also, you can purchase bonds that mature soon (from a few months to a few years) or ones that finish way out into the future ( out to 30 years!). The longer you have your money tied up , the greater the risk that something may happen to the issuer (ex: the company may go bankrupt) and you cannot invest in anything else with that money while it is invested in the bond (opportunity risk) . As before, in theory, the longer the duration of the bond, the higher the interest payment you can receive because of the additional risk involved.

Why diversification is important

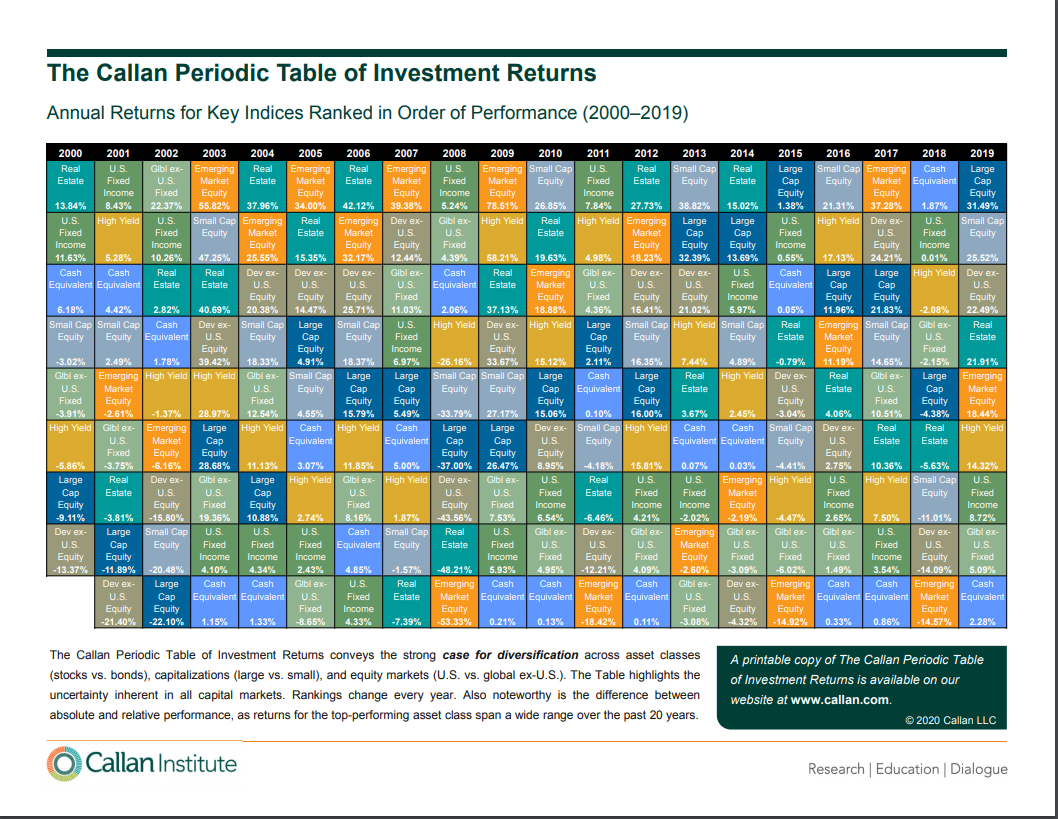

Just like with trying to time the market, trying to predict which asset classes will perform best/worst in any given year is a near impossible task. See below a periodic table of investment returns from The Callan Institute:

Do you see any pattern? Year after year some asset classes will perform well, and others not as much. Sometimes an asset class will experience years of outperformance, and other years of underperformance before having a “good” year. The only way to ensure you can participate in an asset class performing well (or avoiding being clobbered when it is not) is to diversify your investments among a variety of different asset classes. This is why we strongly advocate diversifying your investments in your portfolio.

Why you should continually stay invested

Just like the stock market as a whole, certain asset classes can increase rapidly on a dime. If you are not in vested in that asset class when it jumps, you may have missed a sizable portion of its long-term returns. Over the last few years, large US companies have been the dominant stock performer in the marketplace . One of the main recent laggards have been US small value companies. Using the Exchange Traded Fund IVV as a proxy for the S&P 500 and IJS as a proxy for small US value, IVV was up over 18% in 2020 while IJS was only up 2.6%. However, if you look at the last quarter of 2020, IVV was up 12.2% while IJS was up 32.8%!

If you had sold out of all your small value companies, you would have missed a rapid rise in this asset class in just a few months’ time and your annual performance would have been much worse . This is not to say that this performance will continue in the future, but to emphasize the importance of staying diversified not only in terms of stocks vs bonds, but also by asset class and various sub-categories. Having a well-diversified investment portfolio across the board is one of the best ways to reduce your overall risk, and ensure you are capturing many aspects of the marketplace. If you try to time certain asset classes, you run the risk of missing a big run up or being over exposed during a large drop. We find the best way to manage investments is to have targets of various asset classes and sub-categories and staying invested in them to reduce your risk and participate in any price increases.

Summary

Managing an investment portfolio can be a lot of work. From determining asset classes and how much to hold of each, to continually monitoring and rebalancing , there is much to consider. But having a properly diversified portfolio is one of the best ways to reach your long-term saving goals. Being invested in various asset classes and subcategories allows you to spread out some risk with your investments, while also allowing you to experience some of the price increases in certain areas, especially when they happen quickly. If you need assistance with your overall investment strategy or financial plan, please reach out to our team .