There’s financial incentive for Americans to give generously to charity: when you donate to an IRS-qualified 501(c)(3) public charity, including Fidelity Charitable, you are able to take an income tax charitable deduction. The purpose of charitable tax deductions are to reduce your taxable income and your tax bill—and in this case, improving the world while you’re at it.

1. How much do I need to give to charity to make a difference on my taxes?

Charitable contributions to an IRS-qualified 501(c)(3) public charity can only reduce your tax bill if you choose to itemize your taxes. Generally, you’d itemize when the combined total of your anticipated deductions—including charitable gifts—add up to more than the standard deduction.

Keep track of your charitable contributions throughout the year and consider any additional applicable deductions. Generally, taxpayers use the larger deduction, standard or itemized, when it’s time to file taxes.

2. What can I take a tax deduction for?

In order to take a tax deduction for a charitable contribution to an IRS-qualified 501(c)(3) public charity, you’ll need to forgo the standard deduction in favor of itemized deductions. That means you’ll list out all of your deductions, expecting that they’ll add up to more than the standard deduction.

The most common expenses that qualify are:

- Mortgage interest

- State and local tax

- Charitable giving

- Medical and dental expenses

3. What’s the maximum amount I can claim as a charitable tax deduction on my taxes?

When you donate cash an IRS-qualified 501(c)(3) public charity, you can generally deduct up to 60% of your adjusted gross income. Provided you’ve held them for more than a year, appreciated assets including long-term appreciated stocks and property are generally deductible at fair market value, up to 30% of your adjusted gross income. Combining more than one type of asset can be a tax-efficient move to maximize the amount that you can take as a charitable tax deduction.

4. What do I need in order to claim a charitable contribution deduction?

Once you’ve decided to give to charity, consider these steps if you plan to take your charitable deduction:

- Make sure the non-profit organization is an IRS-qualified 501(c)(3) public charity or private foundation.

- Keep a record of the contribution (usually the tax receipt from the charity).

- If it’s a non-cash donation, in some instances you must obtain a qualified appraisal to substantiate the value of the deduction you’re claiming.

- With your paperwork ready, itemize your deductions and file your tax return.

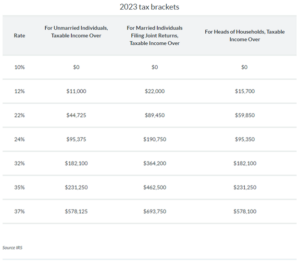

5. Which tax bracket am I in and how does that impact my deductions?

Federal tax brackets are based on taxable income and filing status. Each taxpayer belongs to a designated tax bracket, but it’s a tiered system. For example, a portion of your income is taxed at 12%, the next portion is taxed at 22%, and so on. This is referred to as the marginal tax rate, meaning the percentage of tax applied to your income for each tax bracket in which you qualify. In essence, the marginal tax rate is the percentage taken from your next dollar of taxable income above a pre-defined income threshold. That means each taxpayer is technically in several income tax brackets, but the term “tax bracket” refers to your top tax rate.

6. How does the Pease limitation affect my tax deduction?

The Tax Cut and Jobs Act of 2017 removed the Pease limitation from the tax code. The Pease limitation was an overall reduction on itemized deductions for higher-income taxpayers. The rule reduced the value of a taxpayer’s itemized deductions by 3% of adjusted gross income (AGI) over a certain threshold. The 3% reduction continued until it phased out 80% of the value of the taxpayer’s itemized deductions.

7. Can I take a Fair Market Value deduction for donating private S-corp or C-corp stocks to charity?

Yes, it’s possible to deduct the full fair market value of the contribution if the recipient organization is a public charity. But tactically, the answer depends on whether the charity is able to accept private stock as a gift. Most charitable organizations simply don’t have the resources, expertise or appetite to efficiently accept and liquidate these types of assets, particularly in a time crunch at the end of the year.

However, Fidelity Charitable has a team of in-house specialists who work with donors and their advisors to facilitate charitable donations of S-corp and private C-corp stock every day (among many other assets). Once you make a donation to Fidelity Charitable and the asset is sold, you’re able to recommend grants to your favorite charities, quickly and easily.

And by donating private stock, you generally do not pay capital gains taxes on Fidelity Charitable’s subsequent sale of the stock. There’s a second tax benefit as well: you’ll generally be able to deduct the full FMV as determined by a qualified appraisal.

Reposted from Fidelity Charitable at https://www.fidelitycharitable.org/guidance/charitable-tax-strategies/charitable-tax-deductions.html .

The tax information provided is general and educational in nature, and should not be construed as legal or tax advice. Fidelity Charitable does not provide legal or tax advice. Content provided relates to taxation at the federal level only. Charitable deductions at the federal level are available only if you itemize deductions. Rules and regulations regarding tax deductions for charitable giving vary at the state level, and laws of a specific state or laws relevant to a particular situation may affect the applicability, accuracy, or completeness of the information provided. As a result, Fidelity Charitable cannot guarantee that such information is accurate, complete, or timely. Tax laws and regulations are complex and subject to change, and changes in them may have a material impact on pre- and/or after-tax results. Fidelity Charitable makes no warranties with regard to such information or results obtained by its use. Fidelity Charitable disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Always consult an attorney or tax professional regarding your specific legal or tax situation.

Disclaimer: This is not to be considered investment, tax, or financial advice. Please review your personal situation with your tax and/or financial advisor. Milestone Financial Planning, LLC (Milestone) is a fee-only financial planning firm and registered investment advisor in Bedford, NH. Milestone works with clients on a long-term, ongoing basis. Our fees are based on the assets that we manage and may include an annual financial planning subscription fee. Clients receive financial planning, tax planning, retirement planning, and investment management services and have unlimited access to our advisors. We receive no commissions or referral fees. We put our client’s interests first. If you need assistance with your investments or financial planning, please reach out to one of our fee-only advisors. Advisory services are only offered to clients or prospective clients where Milestone and its representatives are properly licensed or exempt from licensure. Past performance shown is not indicative of future results, which could differ substantially.